EducationStaff WriterTue 03 Oct 17

East Coast Office Markets Rebound in Third Quarter

The third quarter in 2017 saw a mild convergence across east coast office markets, as Sydney and Melbourne growth moderated from strong gains in 2016, while Canberra and Brisbane picked up pace.

"A different picture is starting to emerge compared to six months ago," Cushman & Wakefield head of office leasing Tim Molchanoff said.

“In Sydney, big deals were a key driver this quarter as major tenants moved to take up space in the CBD. In Melbourne, the big landlords competed for pre-commitments as major office developments continued at pace.

“For Brisbane, the recovery continues with vacancies modestly tightening in the prime market with tenant favourable conditions driving office upgrades, while Canberra saw the completion of Cromwell’s 30,000 square metre A-grade Tuggeranong development," he said.

Cushman & Wakefield recently released their third quarter market research for Australian east coast offices, which covered Sydney, Melbourne, Brisbane and Canberra.

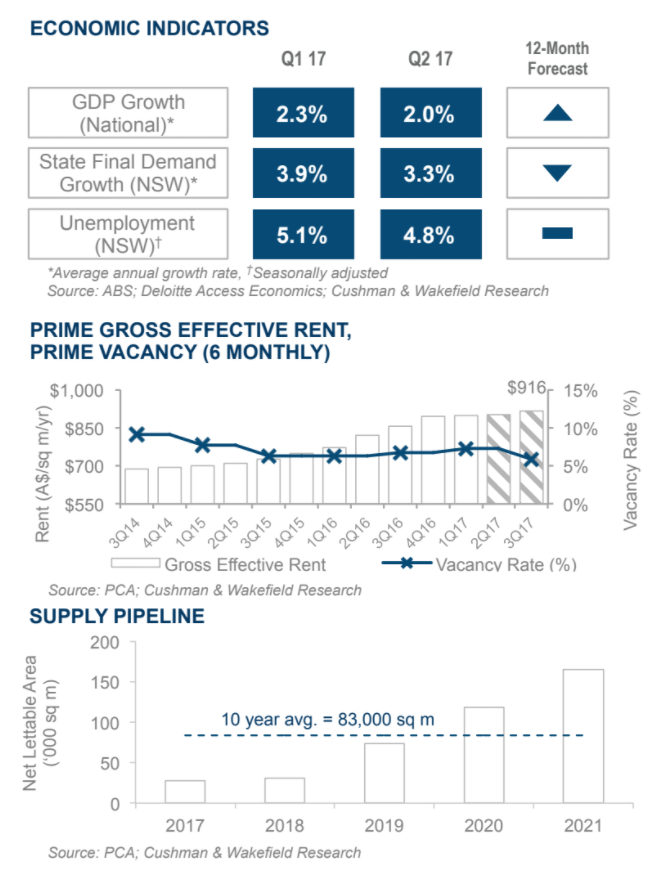

Sydney

After a second quarter in which smaller deals dominated the Sydney CBD office leasing market, the third quarter rebounded with multiple large deals.

The trend of above-average prime-grade net absorption continued with half-year H1 2017 marking the sixth consecutive half-year of above average take-up of stock. On this uptake, vacancy declined, with the premium rate compressing 300 basis points to 9.5 per cent while the A-grade market, down 50 basis points to 3.6 per cent, recorded its lowest rate since mid-2008.

Cushman & Wakefield head of NSW office leasing Tim Courtnall said larger deals have returned to the CBD office market this quarter after Q2 was punctuated by smaller transactions.

"Rental growth in the B-Grade market continues to outpace Premium grade stock, but the gap is narrowing as growth slows. Tenant demand remains strong for suites and subdivided floors, especially from service industries such as Legal, Finance and Technology," he said.

After muted gross effective rental growth in the second quarter, stronger growth returned in the third quarter. Prime gross effective rents, which were up 1.6 per cent q-o-q and 6.9 per cent y-o-y, were underpinned by an increase in face rent growth and a 50 basis point decline in incentives to move to $916 per square metre per annum. B-grade gross effective rents tracked sideways at $729 per square metre with face rent growth stabilising, while gross incentives remained at circa 20 per cent.

“The quarter saw major tech tenants continue to gravitate to the CBD, led by Jobs for NSW establishing their Sydney Start-up Hub, taking 17,000 square metres of refurbished space at Wynyard Green, Dimension Data securing 6,000 square metres at Darling Park, and Atlassian taking additional space at 363 George Street," Courtnall said.

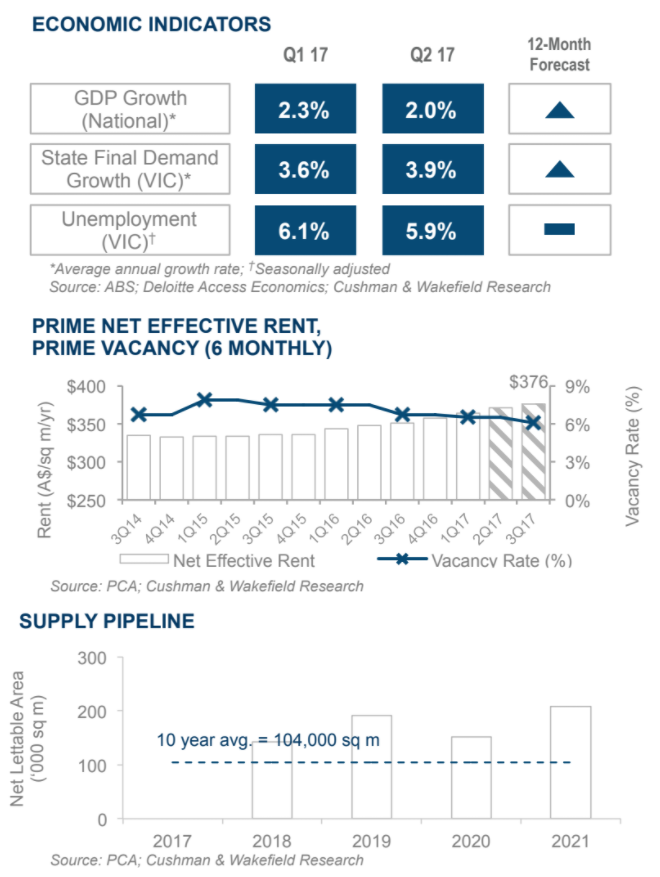

Melbourne

In the third quarter, tenant outgoings increased as landlords passed on higher land tax expenses stemming from recent land revaluations. For prime grade outgoings this equated to a q-o-q increase of 7 per cent, while B-grade outgoings increased by 10 per cent. Landlords have also been exposed to increased electricity costs caused by volatility and uncertainty in the electricity market. Unit rates on multi-year electricity supply contracts rose significantly compared to previous years, and these rises have started to flow back to tenants.

Prime vacancy sharpened 40 basis points to 6.1 per cent in the first half of 2017. Although there was a lack of contiguous stock, prime net absorption matched the historic average. Tighter vacancy drove further rent growth, especially for Premium grade assets. Prime net effective rents now sit at $376 per square metre per annum, up 1.2 per cent q-o-q and 6.9 per cent y-o-y.

“As rental growth in Melbourne experiences a moderate softening, we are continuing to see good options available for tenants," Tenant Advisory Group director Josh Langdon said.

"Demand remains healthy, with major landlords vying to secure larger tents with 12 major office towers in development or approved to proceed.

Landlords were seen to be clambering to secure large requirements, and there are pre-commitment rumours aplenty. Placement of such tenants is expected to provide market clarity and backfill opportunities for smaller tenants, which are expected to be active over the coming year.

“We are also seeing landlords looking to pass on higher land tax and rising energy costs, leading to a spike in outgoings for tenants, particularly in the B-grade market," Mr Langdon said.

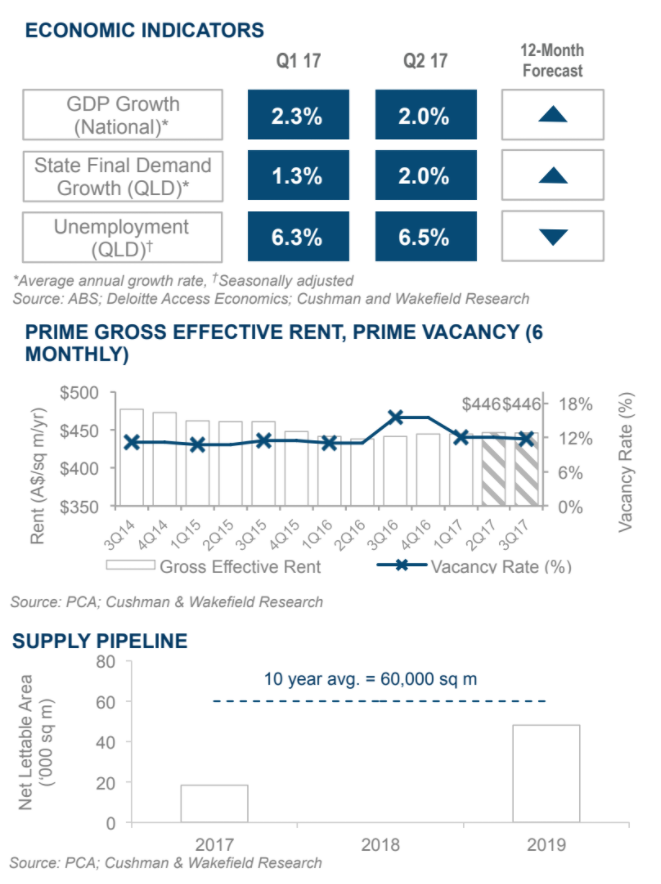

Brisbane

Annual prime net absorption to July 2017 of 111,788 square metres saw the vacancy rate decline from 15.5 per cent to 11.7 per cent. While it was partly driven by the completion of new stock, tenants were also choosing to upgrade office accommodation while the market remains favourable to them.

Prime rents have remained little changed, with 1.1 per cent growth y-o-y on a gross effective basis.

Landlords continued to compete for tenants. Strategies include refurbishing floor space, upgrading building services, and offering speculative fit-outs. The latter became increasingly common and offered smaller-sized tenants a cost-effective turn-key solution.

The Brisbane CBD office market emerged from the worst of the downturn in tenant demand.

Looking to the future, stronger economic growth across most sectors is forecast over the next five years, which, coupled with limited near-term supply and extensive infrastructure projects shaping the CBD, should see the vacancy rate trend downwards. The pace of recovery is expected to gather momentum in 2018 and bring with it stronger rental growth.

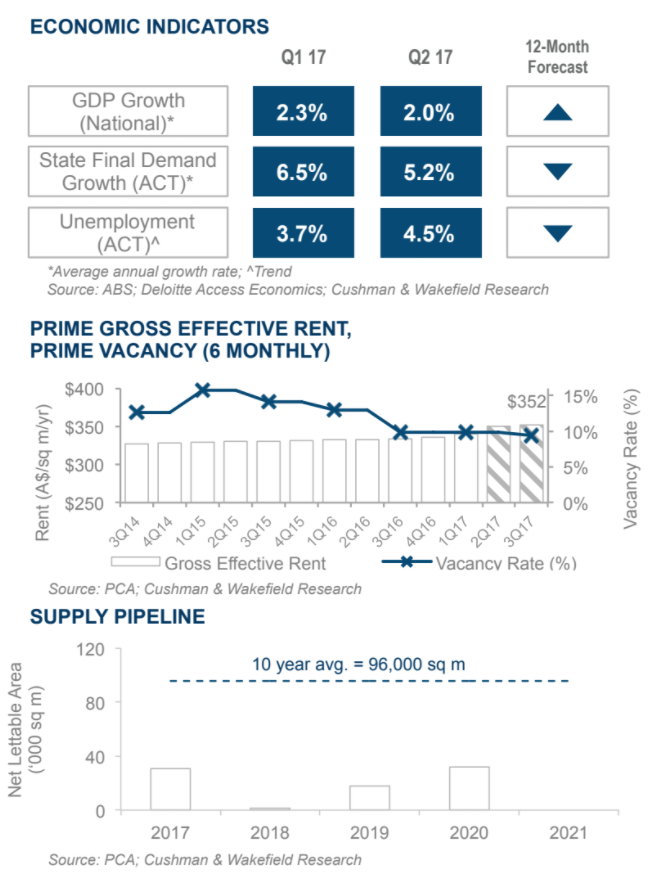

Canberra

In the second quarter, Canberra’s state final demand growth again exhibited strength. The ACT led all service sector-based states, and was second only to the more volatile Northern Territory.

Unemployment in the ACT remained tight at 4.5 per cent and is expected to receive a boost from construction of stage one of the Canberra light rail project, which is now underway.

The Union Court redevelopment at the Australian National University campus forced a number of educational providers to relocate. Landlords on nearby Barry Drive have benefited, with multiple deals reached in the secondary grade circa 500 square metre category.