ResidentialEliza OwenThu 30 Apr 20

Which Rental Markets Are Most Impacted by Covid-19?

Covid-19 is having varied impacts on residential property, but arguably the biggest impact could be in the rental space.

Prior to Covid-19, the Australian rental market was already weak. Now, new challenges are here.

As Australian borders remain closed to tourists, and government policies restrict short-term rental arrangements, Airbnb rentals are converting to long-term rental supply.

The added supply means rents could go down. This is compounded by a decline in demand. Rising job losses are seeing some tenants negotiate lower rents, or find alternative accommodation, such as choosing to move back with parents.

A pause on the flow of international student and migrant numbers could see more properties sitting empty, while domestic students are less inclined to rent close to universities, as they access study remotely.

But the impact on different regions will vary, depending on how exposed markets are to tourism, migration and job losses.

Several datasets point to inner Sydney and Melbourne being the most affected.

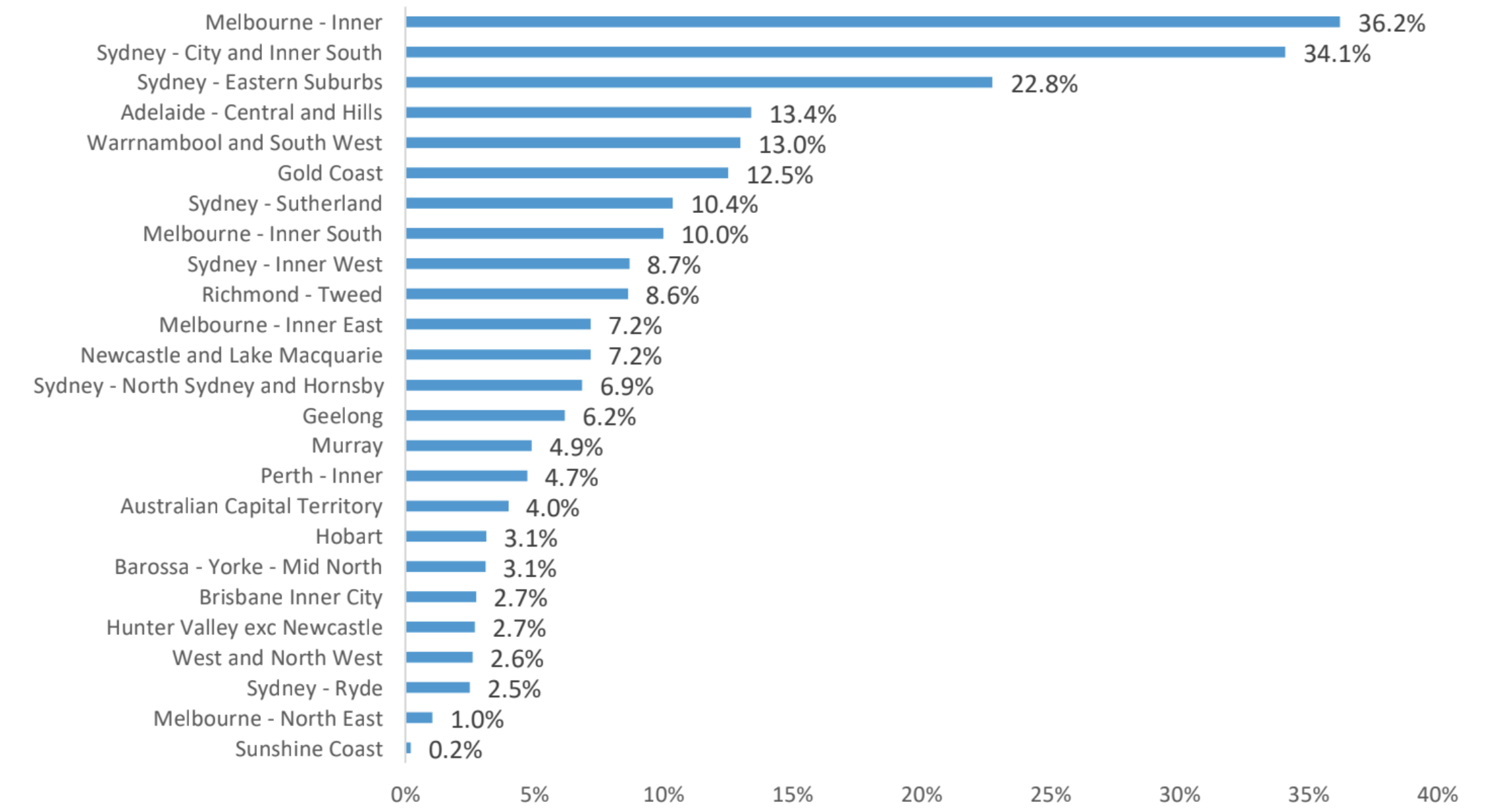

Inner city Sydney and Melbourne to be the hardest-hit rental markets

Preliminary listings data estimates that between the week ending 22nd of March and the week ending 26th of April, the number of properties for rent have increased 0.8 per cent across Australia.

But the most remarkable increases were in the inner-city regions of Melbourne and Sydney, where rental listings have risen over this short period by 36.2 per cent and 34.1 per cent respectively.

The chart below shows the SA4 regions across Australia where rental listings increased over the period following the 22nd of March.

This was around the onset of the strictest lockdowns in business operations, and just after borders were closed to non-residents and non-citizens.

Change in total rental listings by SA4 region - 22nd of March to 26th April

^ Source: Corelogic

As well as elevated levels of recently completed dwellings, part of the reason for higher vacancies in these areas is a negative demand shock from employment and temporary restrictions on migration.

Rental markets are particularly susceptible to declines in overseas migration, because the majority of new migrants seek rental housing upon arrival in Australia.

This will impact Inner Melbourne, which has previously maintained stable rental conditions amid high housing supply, because of rapid growth in international migration.

According to ABS migration data, the Melbourne council region population increased by 8,638 over 2018-19. But 99.5 per cent of this increase was attributable to overseas migration.

This means that new rental demand in this area is almost entirely sourced from overseas migrants.

Areas vulnerable to job loss also have a high portion of renting households

Furthermore, some of the regions in Australia that have been most vulnerable to job loss as a result of Covid-19, are also regions where a high portion of people rent.

This is fairly intuitive when considering the kinds of services and workers that have been most impacted by Covid-19.

A recent ABS survey of changes in employment found that a substantial -25.6 per cent of jobs had recently been lost in accommodation and food services.

Arts and recreation services saw job losses of—18.7 per cent. People employed in these industries, such as hospitality workers, are more likely to be young, and renting.

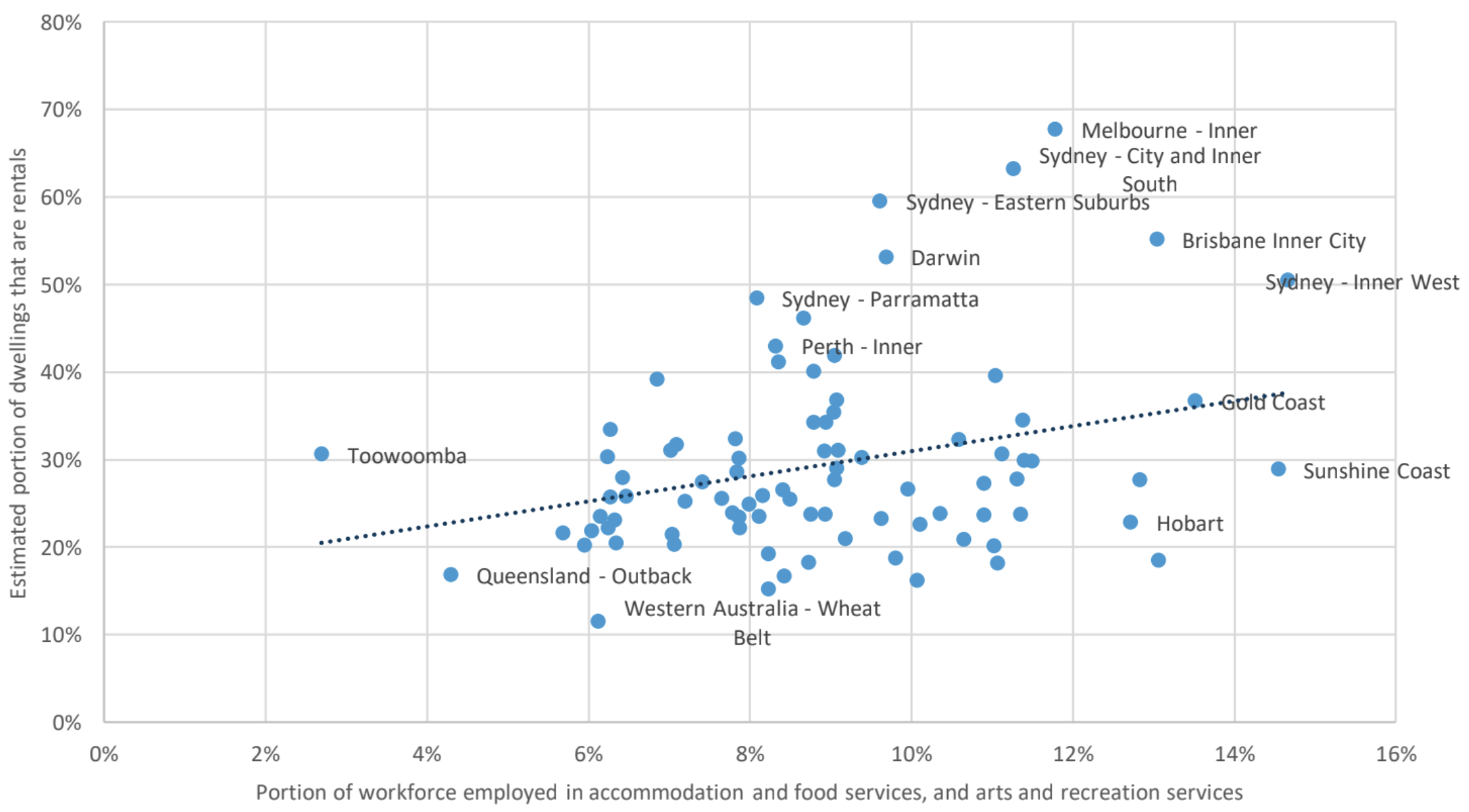

This is also supported by data. The scatter graph below compares two characteristics of SA4 geographies in Australia: the workforce exposure to food and accommodation and arts and recreation (horizontal axis), and the estimated portion of rental dwellings (vertical axis).

Concentration of workforce in industries highly impacted by COVID-19, and portion of renting households - SA4 Regions, Australia

^ Source: CoreLogic, ABS catalogue 6291. Note employment data of the portion of the workforce in arts and tourism is derived from the four quarter average to February 2020

While there is not a perfectly correlated relationship between these industries and renting households, the chart does highlight that Inner Sydney and Melbourne have both a relatively high portion of workers exposed to potential job loss, and renting households.

Inner Brisbane and Sydney’s inner west may also have rental markets with a high incidence of job loss, but so far rental listings have not increased as dramatically.

Between high levels of migration and susceptibility to job loss, inner city Sydney and Melbourne are already experiencing a sharp rise in rental supply.

This will have a range of implications, including the potential for downward pressure on purchase values, an erosion of rental yields and added settlement risk for off-the-plan purchases approaching completion.

For potential renters still in employment, this will also create cheaper accommodation options close to the city.