Resources

Newsletter

Stay up to date and with the latest news, projects, deals and features.

Subscribe

Transaction activity in Australia's retail investment market is set to reach a new record in 2017 as the high rate of turnover for retail assets continues, according the latest research by JLL.

JLL’s annual Shopping Centre Investment Review and Outlook Report revealed an ongoing trend for the last five years, driven by a number of key strategies employed by owners and investors alike.

JLL Head of Retail Investments in Australasia Simon Rooney said investor demand remains very strong from domestic and offshore capital sources.

"Demand continues to outweigh supply of investment product, resulting in surplus capital which is yet to be deployed and driving competition-led yield compression.

“Australia is expected to attract a high proportion of offshore capital again in 2017, given retail yields in Australia remain high in a global context and market fundamentals are relatively stable.

"Australia’s status as a low-risk investment destination with high levels of market transparency and the opportunity to secure large, institutional grade, core and core-plus assets, continues to drive significant demand from global investors.

“Domestic owners will selectively dispose of or offer passive JV interests in assets to fund developments and bolster portfolios, reduce risk and maintain low gearing,” Mr Rooney said.

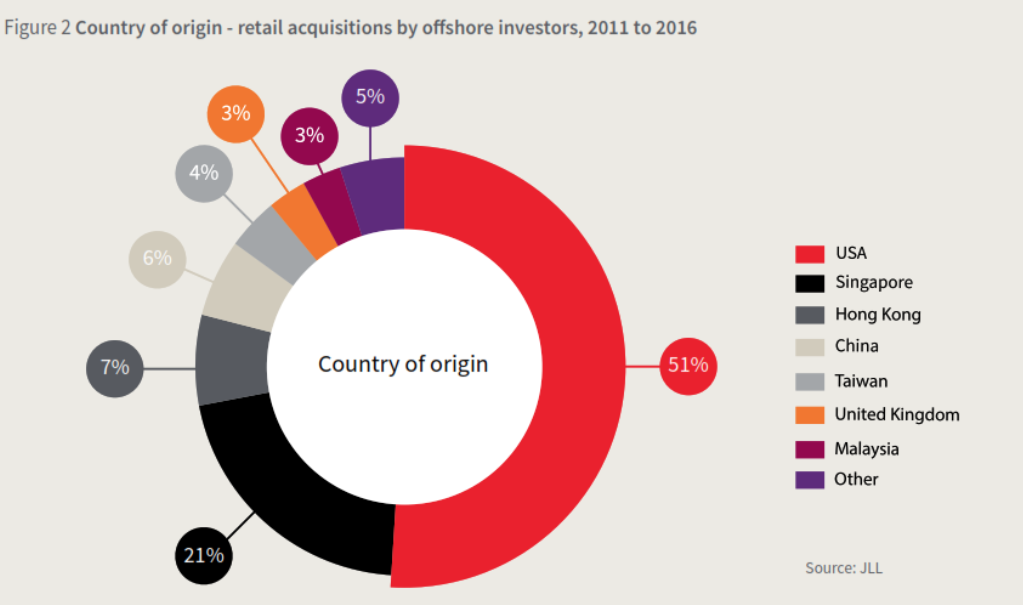

In 2016, transactions to offshore investors reached $2.3 billion, slightly below the $2.5 billion recorded in 2015.

Offshore investment activity accounted for a significant 32% of total acquisitions, compared with the long-term average of 12%.

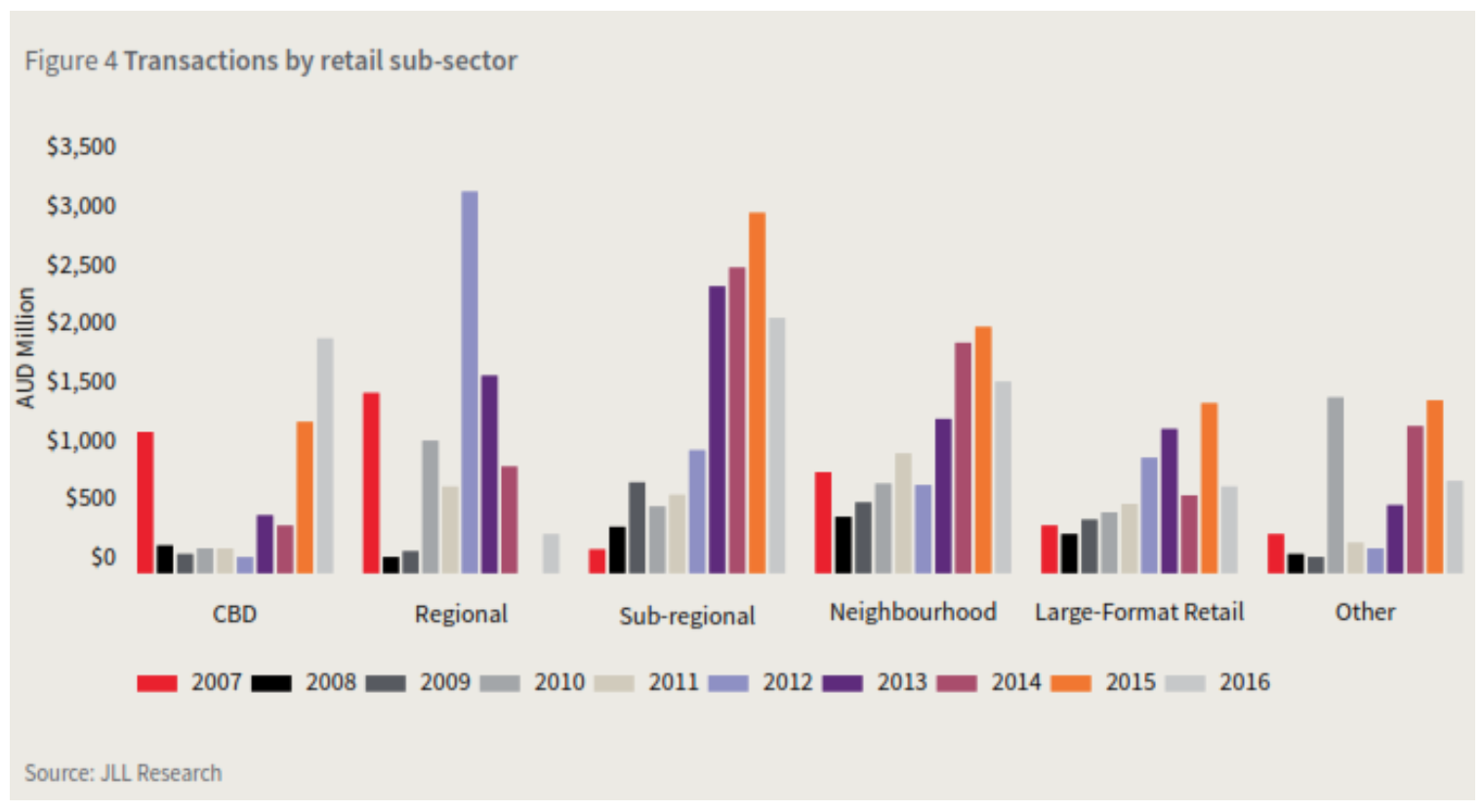

The report said total retail transactions reached $7.3 billion in 2016, down approximately 18% from the record high of $8.9 billion in 2015. CBD and sub-regional shopping centres were the standout performers and the major theme in 2016 – with a record set for CBD shopping centre sales at $1.9 billion. The previous record for CBD transactions was $1.2 billion in 2015.

Sub-regionals accounted for the largest share of activity in 2016 at $2.1 billion (or 28%) and are expected to be the major focus of attention for domestic and offshore investors alike, given their defensive qualities and attractive growth profile.

“Regional shopping centre redevelopments are highly capital intensive," Mr Rooney said.

"We expect a number of major owners to potentially seek diversification by reducing high exposure to a single asset and trade area and look to unlock capital to fund alternative developments across their portfolio.

“Sub-regional assets have been the most highly traded category for each of the last four years. Investors continue to be attracted to this retail sector given their defensive nature and the relative value proposition that it offers in terms of the attractive yields, inbuilt growth and value-add opportunities, to drive returns through active asset management strategies," he said.

Total transactions for neighbourhood centres totalled $1.6 billion in 2016, 41% above the 10 year average. The large majority of transactions occurred in QLD, with 28 transactions totalling $561 million, while neighbourhood centres remained tightly held in NSW and VIC, with only 10 ($524.7 million) and 12 ($248.4 million) transactions.

“Retail fundamentals remain resilient at the headline level," JLL Retail Research Director Andrew Quillfeldt said.

“Owners are deploying capital into their extensive development pipelines and are focused on primarily upgrading and extending existing shopping centres in order to attract and retain tenants, and drive investment returns," he said.

“Although the leasing market has been supported by the entrance of new international brands in certain segments, competition remains high in the retail sector and there is a divergence occurring between the performance of individual retailers.

"Online retailers continue to create further competition for traditional retailers – especially for those that rely on price as a key differentiator.

“Retail turnover growth will be supported over the medium term by a recovery in wages growth and inflation," Mr Quillfeldt said.

"We expect rents to grow at around the rate of inflation through 2017, but are expecting there to be more scope for rents to recover from 2018 given the reset in occupancy cost ratios that has already occurred and the alignment between retail sales growth and fixed rental increases."