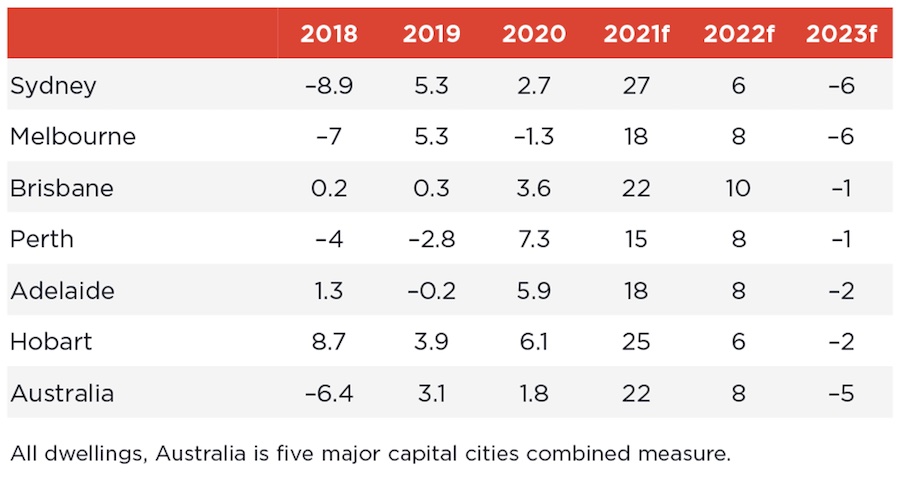

^ Source: Corelogic

Easing border restrictions and the eventual return of overseas students, immigrants and hospitality workers, as well as businesses and nightlife, are expected to rapidly boost demand for city accommodation as has already happened in London, New York and other cities.

Domain’s chief of research and economics Nicola Powell says the capital city CBD markets that have seen the worst impacts of the pandemic will recover the fastest.

“We know that the majority of people arriving from overseas choose Sydney or Melbourne as their destination, she said.

“I think we will see additional pressure on rental markets in Melbourne and Sydney once overseas migration goes back to normal.”

At the same time, buyers are seeing greater value in units due to house price affordability constraints, and growing investor activity is supporting unit prices.

Investor mortgage demand has increased from a record low of around 23 per cent to more than 30 per cent, and CoreLogic head of research Tim Lawless says this is helping to drive recovery in these markets.

“Both the lower entry point and higher yield profile may be an attractive option for investors as they become more active in the housing market,” Lawless says.

CoreLogic tips Melbourne to experience Australia’s highest rental demand growth as international borders open. QBE highlights Geelong as a medium-term growth point, due to its affordability advantage over the state capital.

Exodus to the regions reversing

Another trend expected to develop over coming months is a flow of property buyers from regional areas back to the capital cities.

Living regionally and working remotely will prove less tenable than some recent migrants had expected. Longer-term city dwellers will seek to return to a larger choice of amenities, family and friends, SQM Research director Louis Christopher said. This will add to demand for stock in urban areas.

“I’m expecting to see a swing back towards the cities over time and there will be a move away from the regions,” he said.

“I think the outflow will probably come more from inland Australia rather than the coast, as the coast tends to have more amenities and offer better lifestyle options.”

South-east Queensland popularity to remain

Brisbane, the Sunshine Coast and Gold Coast should continue to experience sustained interstate migration through to 2024, says QBE, as south-east Queensland will remain relatively affordable when compared to Sydney and Melbourne.

Since September last year, 11 per cent of all capital city residents migrating to regional areas have moved to the Gold Coast, making it the most popular destination in Australia according to the Regional Australia Institute.

Work-from-home changing residential needs

Within cities, the continued popularity of working from home will benefit metro areas and regional suburbia.

Managing director of The Demographics Group, Bernard Salt, expects ‘upgraders’ in the 37-45 age group to be the most rapidly growing segment of the residential property market over the next five years.

“I think we will see heightened demand for upgrader McMansion product on the city’s edge (the Zoom call has killed commuting) and/or in idyllic lifestyle locales within striking distance of capital-city workplaces. family-friendly housing: three-to-four bedrooms, two bathrooms, front garden, backyard,’’ says Salt.

Property developers turning to non-bank lenders

Seeking to take advantage of the growing market, property developers are fast tracking projects and acquiring new opportunities in all sectors of the residential property market.

Head of lending and property assets at Trilogy Funds Clinton Arentz says that the Trilogy Funds lending team has been receiving enquiries across Queensland, New South Wales and Victoria from brokers and their developer clients for a large variety of projects.

Whether it is for industrial construction, residential construction or completed stock, inner-city or regional, Trilogy Funds is available to discuss your project finance needs.

“To finance their projects, developers and their brokers are turning to non-bank lenders, who are typically more flexible in their approach and can respond to the changing property market trends,” he said.

Arentz said that while there had also been an increase in the number of non-bank lenders available, brokers should consider more than just the headline rate when comparing their options.

“As a former property developer, I can say from experience that not all lenders are the same,” he said.

“In addition to the rate, I would also suggest working with a lender who has deep experience in the industry, funds available when you need them, personal service and the ability to tailor the loan to your project.”

Trilogy Funds, Arentz said, typically responds within just 48 hours to a well-documented loan application, providing an indication of support as well as proposed terms.

“We provide property development and construction finance between $3 million and $30 million to the residential, commercial, industrial, and retail property sectors,” he said.

“With funds readily available from our pooled mortgage fund, new loans can be settled quickly after approval and timely drawdown payments are made throughout the life of a property development or construction project.

“Unlike the ‘big four’ banks, we are less focused on presales and more interested in property development experience, reputation and quality of the business and marketing plans.”