Could Household Debt Trigger Another Round of Credit Tightening?

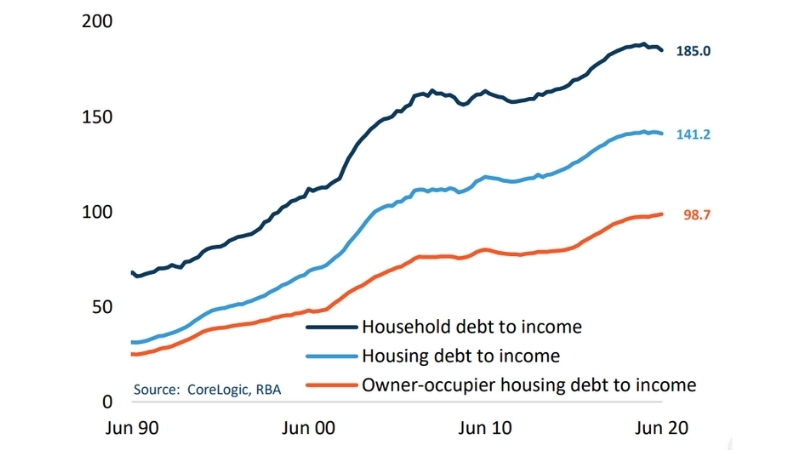

Australian household debt levels have increased substantially over the past three decades, the ratio of household debt to annual disposable income rising from 68 per cent in June 1990 to a recent peak of 188.5 per cent in June 2019.

Since June last year, the ratio has reduced slightly to 185 per cent.

Most of the debt held by households is housing debt, which comprises around 76 per cent of overall household debt.

Thirty years ago housing debt comprised a much smaller 46 per cent of overall household debt.

The skew towards housing debt can also be seen in the latest Household Income and Wealth survey from the Australian Bureau of Statistics.

It showed the median value of debt held against owner-occupied dwellings was $102,600, compared with a median debt level of $5,000 for student loans, $3,000 on credit cards and $3,700 on car loans.

Household, housing debt to income ratio

^ Source: CoreLogic, RBA

Most of Australia’s household debt accrual occurred between 1990 and 2010.

The ratio of household debt to income increased by 45.7 percentage points between 1990 and 2000, and by another 49.3 percentage points between 2000 and 2010.

The past decade has seen growth in the ratio more than half to 21.5 percentage points, with most of that growth aligned with the property boom between late 2012 and 2017.

Importantly, the value of assets held against the debt has recorded a more significant increase, pushing household net worth to new record highs at the end of 2019.

Residential dwellings comprise by far the largest component of household assets, totalling $6.8 trillion, or 53 per cent of household wealth.

Household debt levels are important for two reasons.

Heavily indebted households are generally more vulnerable to a shock such as job loss, illness or a sharp rise in the cost of debt, which in turn has implications for financial stability.

The other key area of concern relates to household spending; heavily indebted households may be more likely to save rather than spend during periods of uncertainty or economic hardship.

With around 60 per cent of Australia’s economy dependent on household consumption, a sustained drop in spending activity would have a negative impact on economic growth.

These risks were recently covered in detail by the RBA in a discussion paper released in May this year.

The outcomes of the paper noted the risk to financial stability was likely to be relatively low due moderate loan-to-valuation ratios on residential mortgages.

In separate analysis from the latest Financial Stability Review, the RBA notes that only 3 per cent of Australian mortgages are thought to be in negative equity.

The risks associated with high household debt levels weighing on consumption are more substantial, especially under a scenario where housing prices fell.

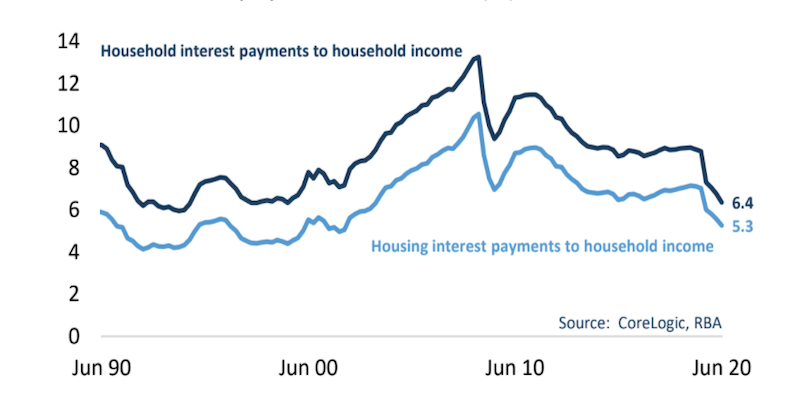

While household debt is high, and potentially a concern for consumption, servicing debt is at its most affordable since 1999 due to record low interest rates.

The ratio of housing interest payments to household disposable income has more than halved since 2008, from a high of 13.3 per cent to 6.4 per cent in June 2020.

With interest rates moving lower since June, it is likely the ratio has fallen even further.

Ratio of interest payments to income

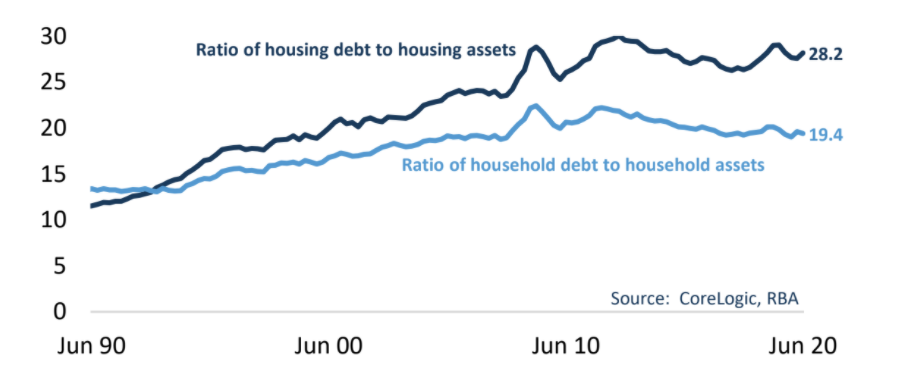

Another factor helping to minimise risk is the fact that

asset values are substantially higher than the debt held

against them.

The ratio of household debt to household assets was 19.4 per cent and the ratio of housing debt to housing assets was 28.2 per cent in June 2020, implying a remarkably large amount of equity is held within the household sector.

Ratio of debt to asset value

Other factors helping to alleviate risk associated with high

household debt, and potentially support a reduction in

debt levels are credit policy and less consumer appetite

for credit.

Lending standards have improved over the past five to ten years, with a trend towards fewer loans originating with a high loan to valuation ratio and substantially fewer interest only loans.

There were 9.2 per cent of home loans originated with a deposit of 10 per cent or less in June this year, down from a recent peak of 22 per cent in 2009.

Similarly, interest-only loans comprised almost 46 per cent of new home loans in mid- 2015, but have averaged only 17 per cent of new lending since mid-2017.

Additionally, loans with a high loan to income ratio have remained low, with June data showing only 5.8 per cent of new home loans were originated with a loan to income ratio of 6 per cent or higher.

It is clear that households became more risk averse through the worst of the Covid period.

National accounts data showed the household saving ratio sky- rocketed to almost 20 per cent through the June quarter, up from 2.5 per cent in the June quarter of 2019.

Given that the virus curve has flattened and consumer sentiment surged in recent months, it is likely the saving ratio will drop.

Additionally, the trend in personal credit, which has been in negative monthly growth territory since late 2019, has plummeted since March.

Although the risks around high household debt are manageable at the moment, interest rates will eventually rise down the track.

As debt servicing costs move higher, a heavily indebted household sector would need to devote more of their income towards servicing debt and less to spending, which implies a medium-to-long term risk to household spending.

This implies high debt levels may also stagger and slow an economic recovery.

If increases in housing debt servicing costs result from higher interest rates, the exacerbated drag on spending could slow economic growth.

Additionally, with household debt remaining high, the sector is more exposed to unforeseen events such as job loss and illness, as well as black swan events like a pandemic or financial crisis.

It is likely policy makers and regulators will be keeping watch for any signs of rising household debt or slippage in lending standards that could lead to higher household debt.

Higher LVR lending or higher loan to income ratios could be the trigger for a new round of macro-prudential style intervention.

Recent macro-prudential interventions targeted interest only lending and growth in lending for investment housing through 2014 and 2019.

Future interventions may be aimed at keeping a lid on household debt levels, and minimising longer-term risk, via firm limits on loan to valuation ratios, loan to income ratios or debt to income ratios.

Power to the Port: Momentum Grows for Northern Adelaide’s Riverside Revival

Borger Warns Sydney’s Olympic Park Risks Missing Housing Moment

‘Maybe in a Decade’: Metricon Chief Executive’s Big Bet

Beyond the Building: Guest Experience Firms as Hotel Gamechanger